FY2025-26 on the ASX: the miners came back and the market darlings broke

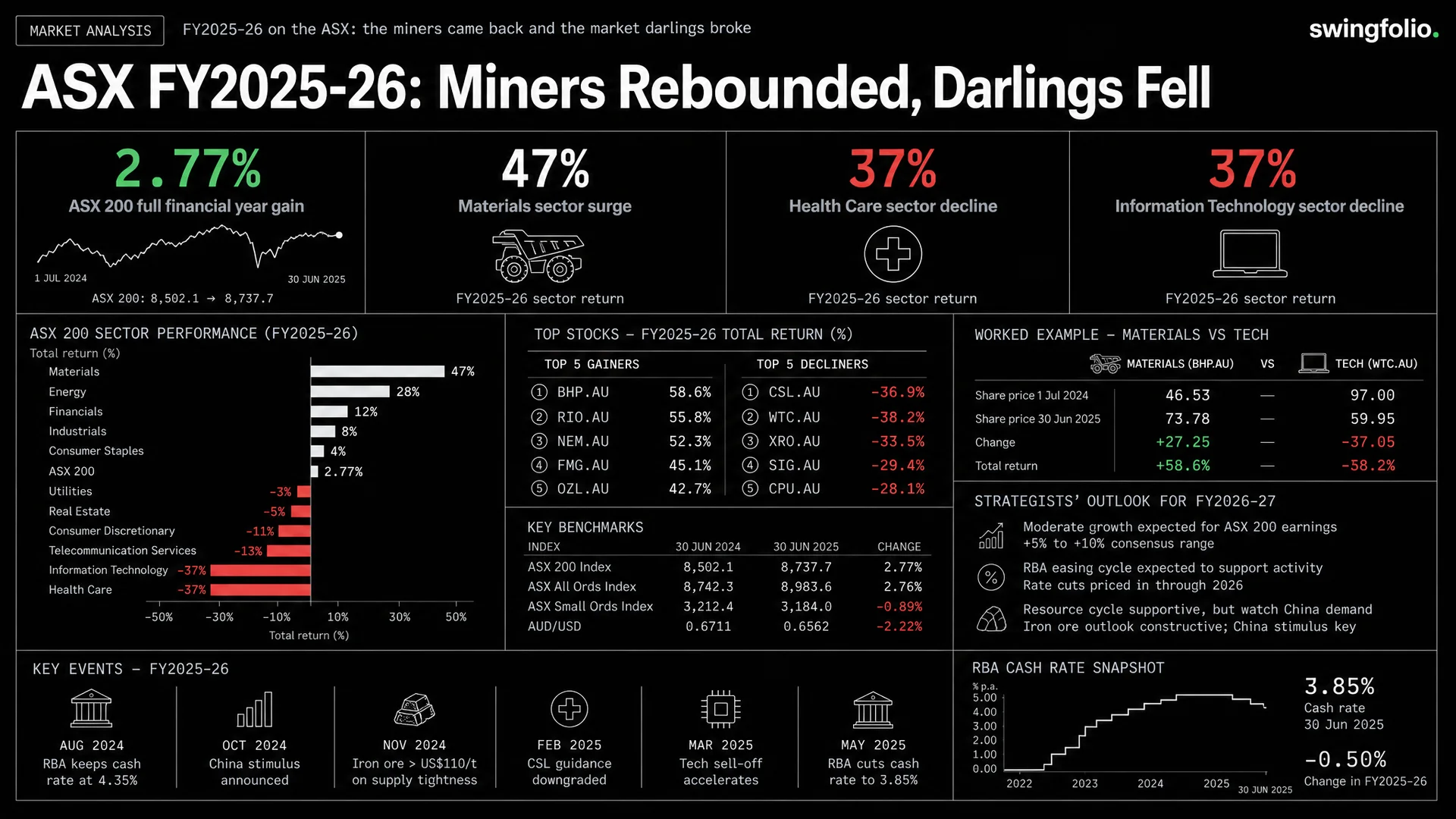

ASX 200 close (30 June 2026): 8,778.7, up 2.77% for the financial year. All Ordinaries: up 2.43%. Small Ordinaries: up 5.46%.

The ASX 200 finished the financial year at 8,778.7, up 2.77% on where it started last July. Add the roughly 3.5% the index pays in dividends and the total return sits near 6%. That is a quiet headline for a year that was anything but.

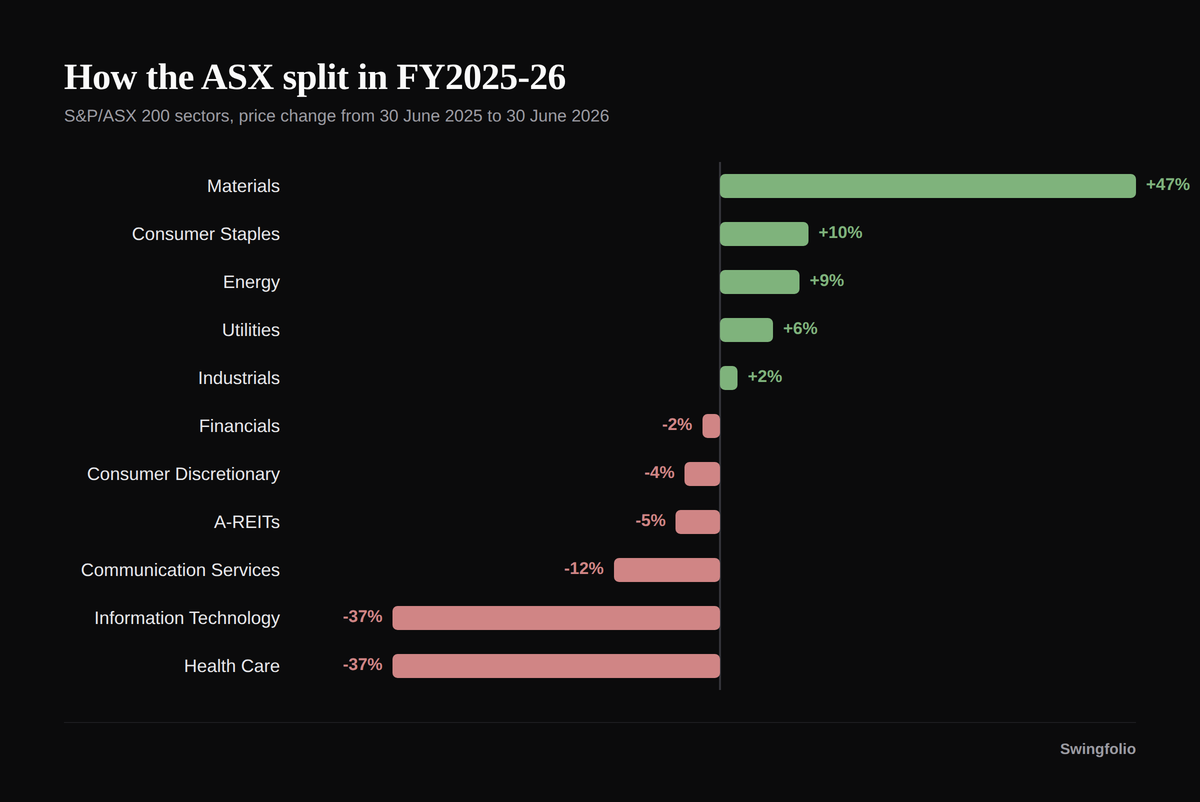

The flat number hides the widest gap between winners and losers in years. Materials rose 47%. Health Care and Information Technology each fell about 37%. Financials, the largest weight on the market, finished down. The same index move can sit on top of a calm year or a sharp rotation. This year it was the rotation.

The year had two halves

The index did not grind higher all year. It ran to a record 9,203 in February 2026, then gave most of it back. A war in the Middle East started in late February, oil ran from about US$70 to roughly US$120 a barrel by April, inflation picked back up, and the Reserve Bank moved from cutting to hiking. Equities stayed calm on the surface for most of the year, with the local volatility gauge sitting near 11 for much of it, but the late shock pulled the index off its high. By 30 June, with oil back below US$80 after a US-Iran agreement in mid-June, the ASX 200 had settled at 8,778.7.

The first half was a mining rally and rate-cut hopes. The second half was rising rates and an oil spike that pulled the index back.

The sector scorecard

The gap between the best sector and the worst was more than 80 points. Money left the long-duration growth names and the high-multiple defensives and went into resources.

The winners: gold, copper and a lithium revival

Materials led the market, up 47%. Gold crossed US$4,000 an ounce for the first time in October 2025, peaked near US$4,400 around Christmas, and eased back below US$4,000 by late June to finish the year up about 22%. Central banks kept buying, the US Federal Reserve cut three times in the back half of 2025, and safe-haven demand added to it. Copper rose about 24%, a supply story more than a demand one: the Grasberg mine disaster in September 2025 removed a chunk of world supply and the London price hit a record near US$13,387 a tonne in January 2026.

The big miners followed the metals. BHP (BHP.AU) rose 61.6%, from $36.75 to $59.40, led by copper, which now makes up close to half its earnings. Rio Tinto (RIO.AU) rose 61.0%. Iron ore, the thing most people still associate with these names, stayed range-bound near US$100 to US$110 a tonne and was roughly flat for the year. The gold miners ran on margin: Evolution Mining (EVN.AU) rose 50.8% and Newmont (NEM.AU) 54.1% as the gold price ran well clear of their cost of production.

Lithium turned hard after two years of being written off. Pilbara Minerals (PLS.AU) rose 276%, Mineral Resources (MIN.AU) 188%, and Core Lithium (CXO.AU) 155%. The trigger was supply, not electric-car demand: a large Chinese lepidolite mine run by CATL was suspended in August 2025 when its permit expired, and the market flipped from surplus to deficit. Battery storage, not electric vehicles, is now the swing buyer.

| Biggest large-cap winners | FY |

|---|---|

| BHP (BHP.AU) | +62% |

| Rio Tinto (RIO.AU) | +61% |

| Newmont (NEM.AU) | +54% |

| Evolution Mining (EVN.AU) | +51% |

| South32 (S32.AU) | +34% |

| Woolworths (WOW.AU) | +29% |

The losers: the expensive names re-priced

The market's most-loved growth and quality stocks had a hard year, and they fell for one reason above all: rates. When bond yields rise, the market pays less for earnings that sit far in the future, and these were the names priced for the most distant earnings.

WiseTech Global (WTC.AU) fell 69.7%, from $109.03 to $33.00. The logistics-software company spent the year in a governance saga: the Australian Federal Police raided it in October 2025 over alleged share trading by its founder, the board churned, and its acquisition of e2open diluted the high margins investors had paid up for. Xero (XRO.AU) fell 59.8% as the global software sell-off met scepticism about its US$2.5 billion Melio acquisition.

Health care was hit just as hard. CSL (CSL.AU), long the bluest of the blue chips, fell 52.1%, from $239.48 to $114.74. At its October 2025 annual meeting it cut profit guidance and pointed to a fall in US flu-vaccination rates under a more vaccine-sceptical US administration. The shares fell about 17% in a day, the worst since CSL listed in 1994. First-half profit then fell 81% on a large writedown, and the chief executive announced his exit. Cochlear (COH.AU) fell 59.5%, most of it in a single April 2026 session after it cut guidance by roughly a quarter. ResMed (RMD.AU) fell 26.6%, weighed by fears that weight-loss drugs reduce demand for its sleep-apnea machines.

It was not only tech and health care. Seek (SEK.AU) fell 44.1% as job-ad volumes kept falling. Treasury Wine Estates (TWE.AU) fell 39.1% after scrapping its full-year guidance in October 2025 on weak Penfolds sales in China. Temple & Webster (TPW.AU) fell 70.9% and was removed from the ASX 200. None of these moves came from a demerger or a one-off accounting quirk. They were genuine re-pricings.

| Biggest large-cap losers | FY |

|---|---|

| Temple & Webster (TPW.AU) | -71% |

| WiseTech (WTC.AU) | -70% |

| Xero (XRO.AU) | -60% |

| Cochlear (COH.AU) | -60% |

| CSL (CSL.AU) | -52% |

| Seek (SEK.AU) | -44% |

The banks: CommBank's year, and the budget

The banks split. ANZ (ANZ.AU) rose 21.2% on a cheap starting valuation and a turnaround under new management. Commonwealth Bank (CBA.AU) fell 10.9%. It began the year as the most expensive major bank in the developed world, near 27 times earnings, and the premium unwound as money rotated into miners.

On 13 May 2026 the Federal Budget abolished the 50% capital-gains-tax discount on shares and investment properties and wound back negative gearing. As the country's biggest mortgage lender, CBA fell more than 10% that day, its largest one-day fall on record, and pulled the other banks down with it. That policy change is the biggest structural shift for Australian investors heading into the new year, and it reaches well beyond bank shares.

Rates went up, not down

The story most people expected at the start of the year was rate cuts. The opposite happened. The Reserve Bank cut once, to 3.60% in August 2025, then reversed: it hiked in February, March and May 2026 to finish the year at 4.35%, the highest cash rate since 2012 and the highest in the developed world. Inflation had climbed back above the 2 to 3% target band, helped by the oil spike. The Australian dollar rose almost 5% to about 69 US cents, mostly because the Reserve Bank was raising rates while the US Federal Reserve had stopped cutting.

Higher rates explain the rotation. They punished the expensive growth and health-care names and supported the move into resources and into companies that pay cash now.

What's expected for FY2026-27

Morgan Stanley set a 12-month ASX 200 target of 9,250 on 19 May 2026, about 8% above where the year ended, on the view that mining and energy earnings can offset a slowing consumer. Earlier targets near 8,900 from UBS and AMP were set in late 2025, before the Middle East shock, so they read as dated now. Others are more cautious: Cadence Capital said a flat year would be a good outcome given the risks.

On rates, the debate has shifted from "more hikes" to "when do cuts start." Commonwealth Bank and NAB both expect cuts during 2027, to 3.85% and 3.60% respectively. Westpac is the outlier, pencilling in two more hikes first.

On sectors, strategists are mostly underweight the banks, which are still expensive, and prefer resources, which trade at a large discount to the rest of the market. Health care is the contested one. After the de-rating, some analysts now see value in the fallen names and call CSL cheap relative to its own history. Morningstar holds a fair value on CSL near $165 against a price below $115. Others think the policy and pricing pressure is structural and not done.

On commodities, gold is still the high-conviction call, with J.P. Morgan looking for close to US$6,000 an ounce by late 2026. Copper is structurally tight. Lithium's recovery is real but distrusted. Iron ore is the laggard most expect to fall toward US$75 to US$90 a tonne as new supply from Guinea's Simandou mine ramps up.

The risks are well flagged: an AI and technology valuation bubble that could correct, the durability of the Middle East ceasefire and the oil price, inflation staying sticky enough to keep rates high, and China's demand for iron ore. The Australian dollar, near 69 cents, tends to move as a proxy for all of it.

The one-line version

FY2025-26 was a split market. The index barely moved, but the miners had one of their best years in a decade while the market's favourite growth and health-care names lost half their value. The cause was the thing nobody expected at the start: rates went up, not down. Whether the new year repeats the rotation or reverses it depends on oil, inflation and the Reserve Bank.

General information only. Not financial advice. Past performance is not a guide to future returns. Track your own trades and performance with Swingfolio.