The 12-Month Rule in Plain Terms

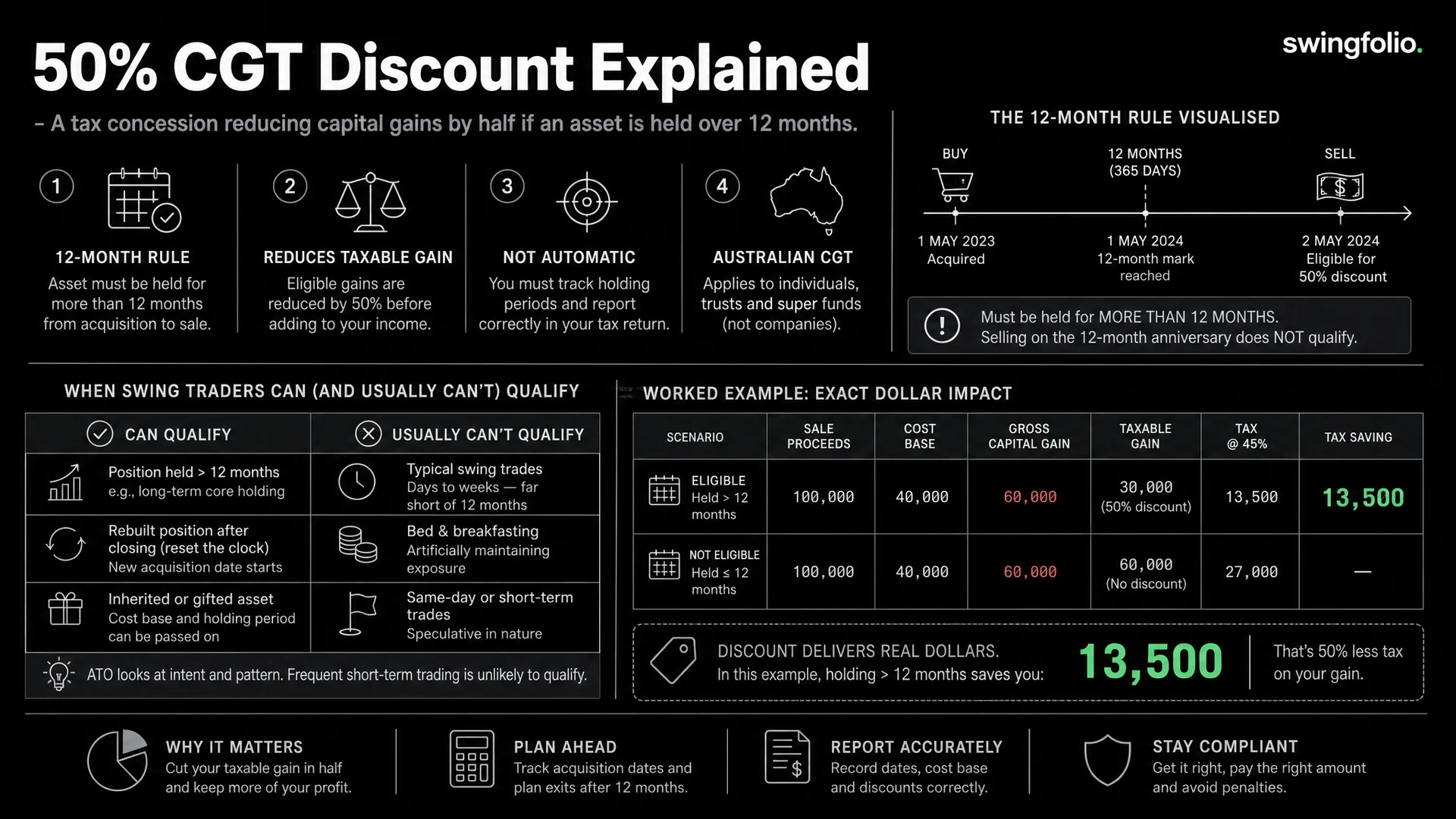

If you hold a CGT asset for at least 12 months before selling, you can reduce your capital gain by 50% before including it in your taxable income. This is the individual CGT discount, and it is one of the most significant tax benefits available to Australian investors.

The catch for active traders: you need to hold the asset for a minimum of 12 months. Not 365 days -- the ATO measures it as 12 calendar months plus one day. If you buy on 1 March 2025, you must sell on or after 2 March 2026 to qualify. Selling on 1 March 2026 does not qualify.

For swing traders whose typical holding period is 2 days to 6 weeks, the 50% discount is almost never available. But understanding exactly how it works helps you recognise the rare situations where it can apply and plan accordingly.

How the Discount Calculation Works

The discount is applied after capital losses have been offset against gains -- not before. This ordering matters and is a common mistake in tax calculations.

Here is the correct sequence:

- Calculate your total capital gains for the year (both discounted and non-discounted)

- Subtract any current-year capital losses from your total gains

- Apply any carried-forward capital losses from prior years

- Only then apply the 50% discount to the remaining gains that qualify

Worked Example: The Ordering Trap

Scenario: You made a $10,000 capital gain on a stock held for 14 months (qualifies for discount) and a $4,000 capital loss on a short-term trade.

Correct calculation (ATO method):

- Gross capital gain: $10,000

- Less capital loss: -$4,000

- Net gain before discount: $6,000

- Apply 50% discount: $6,000 x 50% = $3,000

- Net capital gain included in taxable income: $3,000

Wrong calculation (common mistake):

- Gross capital gain: $10,000

- Apply 50% discount first: $10,000 x 50% = $5,000

- Less capital loss: -$4,000

- Net capital gain: $1,000 (this is wrong and will get flagged by the ATO)

The difference is $2,000 in taxable income. At the 37% marginal rate, that is $740 in additional tax. The ATO's method reduces the gain before applying the discount, which produces a less favourable result for the taxpayer.

Why Most Swing Traders Miss the Discount

The maths is straightforward. If your average holding period is 5-20 trading days, you will never meet the 12-month threshold on those trades. Typical swing trading statistics for active ASX traders:

- Average hold for winning trades: 8-15 trading days (roughly 2-3 calendar weeks)

- Average hold for losing trades: 3-7 trading days (stopped out faster)

- Percentage of trades held over 12 months: less than 2%

Across 100 swing trades in a year, perhaps 1-2 might accidentally qualify for the discount. The other 98 trades are taxed at your full marginal rate on the entire capital gain.

This is not a reason to change your strategy. Holding a stock for 12 months to qualify for the discount when your analysis says to sell at 3 weeks defeats the entire purpose of swing trading. The discount saves you 50% on the gain; holding too long can cost you 100% of the gain if the price reverses.

Edge Cases Where Swing Traders Do Qualify

Despite the typical short holding periods, there are legitimate situations where a swing trade ends up qualifying for the CGT discount:

The Stuck Position

You enter a swing trade expecting a 2-3 week hold. The stock moves against you but does not hit your stop loss. It then goes sideways for months. Eventually, after 13-14 months, it rallies back to your target and you exit at a profit.

This is the most common way swing traders accidentally qualify. The gain is often modest (you waited a long time for a small profit), but the 50% discount applies to whatever that gain is.

The Scale-Out That Goes Long

You buy 1,000 shares of FMG.AU at $18.50 and sell 700 shares three weeks later at $20.80 for a quick profit. The remaining 300 shares you keep as a "free ride" with a stop at break-even. Those 300 shares sit in your portfolio for 14 months before you finally exit at $22.00.

The first exit (700 shares) does not qualify for the discount. The second exit (300 shares) does. Your records need to clearly separate the two exits with their respective holding periods.

The Core-Plus-Swing Approach

Some traders maintain a core long-term position in a stock and trade a swing position around it. For example, you hold 500 shares of CSL.AU as a long-term position and separately buy/sell 200-300 share blocks as swing trades.

The core position may qualify for the discount when eventually sold. The swing trades will not. Parcel identification (covered in our FIFO vs LIFO article) becomes important here to ensure you are selling the swing parcels, not the core holding.

Partial Exits and Holding Period Tracking

When you sell part of a position, each parcel has its own acquisition date and its own holding period. Mixing parcels with different holding periods is where record-keeping gets complicated.

Example:

- 1 Jan 2025: Buy 500 shares of WDS.AU at $26.00

- 15 Jun 2025: Buy 300 shares of WDS.AU at $24.50

- 1 Apr 2026: Sell 400 shares at $28.00

Which 400 shares did you sell? Under FIFO, you sold 400 from the first parcel (held 15 months -- discount applies). Under LIFO, you sold 300 from the second parcel (held 9.5 months -- no discount) and 100 from the first (held 15 months -- discount applies on those 100).

The method you choose changes both the cost base and the discount eligibility. On 400 shares at $28.00 ($11,200 proceeds), the tax difference between these two approaches could be several hundred dollars.

Tracking this manually across dozens of positions gets messy fast. SwingFolio maintains the link between each entry parcel and each exit, calculating holding periods automatically so you can see at a glance which exits qualify for the discount.

Different Discount Rates by Entity Type

The 50% discount only applies to individuals and trusts. Other structures get different treatment:

Individuals: 50% Discount

The standard discount. Available to Australian resident individuals on CGT assets held for over 12 months. Foreign residents lost access to the discount on assets acquired after 8 May 2012 (with some exceptions for property held before that date).

Self-Managed Super Funds (SMSFs): 33.33% Discount

Complying superannuation funds receive a one-third discount, not one-half. The discounted gain is then taxed at the fund's concessional rate of 15%, producing an effective rate of 10% on the discounted portion. Assets in pension phase may be entirely exempt from CGT.

For an SMSF swing trading account, the 33.33% discount is less generous than the individual rate but still meaningful on positions held over 12 months. The 15% tax rate on the remaining gain is much lower than most individuals' marginal rates.

Companies: No Discount

Companies do not receive any CGT discount. All capital gains are taxed at the company tax rate (25% for base rate entities or 30% for larger companies) regardless of how long the asset was held.

If you are trading through a company structure, the 12-month holding period is irrelevant for CGT purposes. Every gain is taxed in full. This is one reason why the choice of trading structure (individual vs company vs trust vs SMSF) has significant long-term tax implications and should be discussed with an accountant before you start.

Tax Planning Around the Discount

While you should not hold positions purely for the discount, there are practical ways to factor it into your decision-making:

Near the 12-month mark: If a position is approaching 12 months and your analysis is neutral (not a strong sell signal), consider waiting the extra few days or weeks to qualify. The discount needs to save more than the risk of holding longer.

Financial year timing: If you have a position that qualifies for the discount and you also have unrealised losses elsewhere, consider crystallising the losses in the same financial year to reduce the discounted gain further.

Record your holding periods: Whether you qualify or not, accurate holding period records are required for your tax return. The ATO expects you to correctly identify which gains qualify for the discount and which do not.

The Dollar Impact in Real Terms

To put the discount in perspective, here is what it means in actual tax savings:

| Capital Gain | Marginal Rate | Tax Without Discount | Tax With Discount | Saving |

|---|---|---|---|---|

| $2,000 | 32.5% | $650 | $325 | $325 |

| $5,000 | 37% | $1,850 | $925 | $925 |

| $10,000 | 37% | $3,700 | $1,850 | $1,850 |

| $20,000 | 45% | $9,000 | $4,500 | $4,500 |

These are meaningful amounts. On a $20,000 gain at the top marginal rate, the discount saves $4,500 in tax. But you had to hold the asset for over 12 months to get it, and the risk of holding that long may have cost you more than $4,500 in potential losses.

The discount is a bonus when it happens naturally. It should not be the driver of your trading decisions.

Disclaimer: This article is general information only and does not constitute financial or tax advice. Tax rules are complex and individual circumstances vary. The examples use simplified calculations and do not account for all possible factors (Medicare levy, HELP debt, offsets, low-income offsets). Always consult a qualified tax professional for advice specific to your situation.