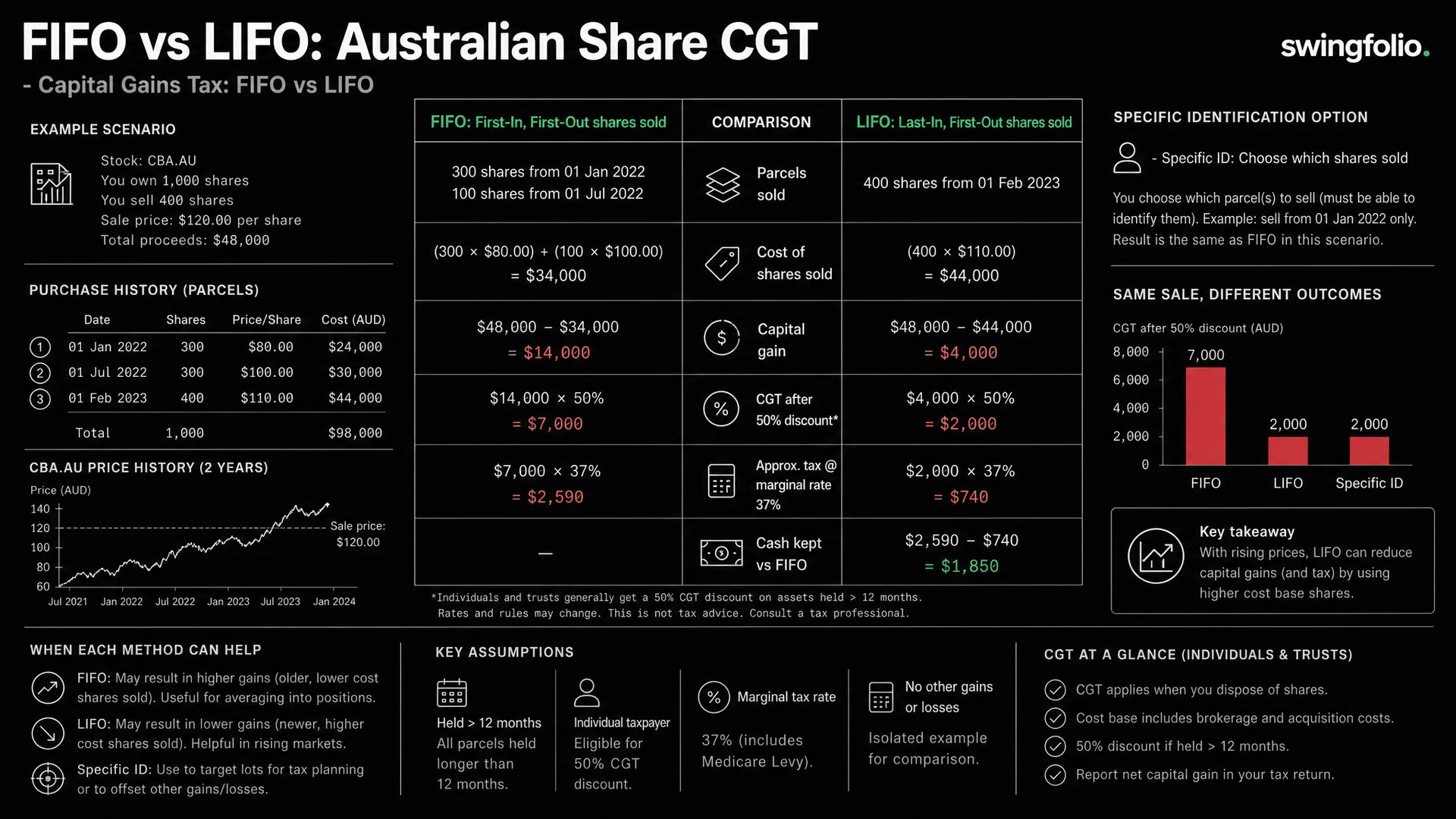

Why Parcel Selection Matters for Your Tax Bill

When you sell shares you have bought across multiple occasions, the ATO needs to know which specific shares you sold. If you bought 500 shares of BHP in January at $42.00, another 500 in March at $38.50, and another 500 in June at $45.00 -- then sold 500 shares in November at $46.00 -- your capital gain changes depending on which parcel you are deemed to have sold.

This is parcel identification, and the method you choose directly affects how much CGT you owe.

The ATO allows three approaches: FIFO (first in, first out), LIFO (last in, first out), and specific identification (you choose exactly which parcel to sell). Each produces a different taxable outcome on the same transaction. The difference can be hundreds or thousands of dollars per trade.

The Three Methods Explained

FIFO (First In, First Out)

FIFO assumes you sell your oldest shares first. Most Australian brokers apply this as the default. When you sell 500 shares, FIFO assigns the sale to the first parcel you purchased, regardless of price.

The advantage of FIFO is simplicity. You do not need to make any decisions at the time of sale. The disadvantage is that FIFO may not produce the best tax outcome, and it removes your ability to optimise.

LIFO (Last In, First Out)

LIFO assumes you sell your most recently purchased shares first. This is less common as a default in Australian platforms, but the ATO accepts it as a reasonable method.

LIFO tends to produce smaller capital gains when a stock has been trending upward (because you sell the highest-cost shares first). It tends to produce larger gains when a stock has been declining, since you sell the cheapest recent shares first.

Specific Identification

Specific identification lets you choose exactly which parcel you sell. The ATO allows this under Taxation Determination TD 33, provided you make the selection before settlement and keep adequate records. This is the most flexible approach and the one that enables genuine tax optimisation.

The requirement is clear: you must identify the specific parcel at or before the time of the transaction, not after the fact when you are doing your tax return. Retrospectively choosing the most favourable parcel is not permitted.

Worked Example: Same Stock, Three Different CGT Outcomes

Let us walk through a concrete example. Assume you are an individual taxpayer in the 37% marginal tax bracket.

Purchases of NAB.AU:

| Parcel | Date | Units | Price | Cost |

|---|---|---|---|---|

| Parcel 1 | 1 Feb 2025 | 300 | $34.50 | $10,350 |

| Parcel 2 | 15 May 2025 | 300 | $31.00 | $9,300 |

| Parcel 3 | 10 Sep 2025 | 300 | $36.80 | $11,040 |

Sale: 300 shares sold on 20 March 2026 at $38.00 = $11,400

Outcome Under FIFO

FIFO sells Parcel 1 (bought 1 Feb 2025 at $34.50).

- Cost base: $10,350

- Proceeds: $11,400

- Capital gain: $1,050

- Holding period: 13 months (over 12 months)

- 50% CGT discount applies: taxable gain = $525

- Tax at 37%: $194

FIFO produces the lowest tax here because Parcel 1 qualifies for the 50% CGT discount and has a moderate cost base.

Outcome Under LIFO

LIFO sells Parcel 3 (bought 10 Sep 2025 at $36.80).

- Cost base: $11,040

- Proceeds: $11,400

- Capital gain: $360

- Holding period: 6 months (under 12 months)

- No CGT discount: taxable gain = $360

- Tax at 37%: $133

LIFO produces a smaller raw gain ($360 vs $1,050), but no CGT discount applies because the holding period is under 12 months. Despite the smaller gain, the tax payable is $133.

Outcome Under Specific Identification

You choose Parcel 2 (bought 15 May 2025 at $31.00).

- Cost base: $9,300

- Proceeds: $11,400

- Capital gain: $2,100

- Holding period: 10 months (under 12 months)

- No CGT discount: taxable gain = $2,100

- Tax at 37%: $777

This would be the worst choice in this scenario. But specific identification does not mean you always pick the most expensive parcel -- it means you pick the optimal one given the full picture.

With specific identification, you would look at all three options and select the one producing the lowest after-tax cost. In this case, you would choose Parcel 3 (the LIFO option) at $133 tax. But the point of specific identification is that you make that decision rather than having a default rule make it for you.

Summary Table

| Method | Parcel Sold | Gain | Discount | Taxable Gain | Tax at 37% |

|---|---|---|---|---|---|

| FIFO | Parcel 1 ($34.50) | $1,050 | Yes (50%) | $525 | $194 |

| LIFO | Parcel 3 ($36.80) | $360 | No | $360 | $133 |

| Specific ID | Your choice | Varies | Depends | Varies | Varies |

In this example, LIFO beats FIFO by $61. Over a year of active trading with dozens of exits, those differences compound.

When FIFO Beats LIFO

FIFO tends to produce a better result when:

-

Your oldest parcels qualify for the 50% CGT discount and the discount effect outweighs a higher raw gain. In the example above, the discounted FIFO gain ($525) was higher than the undiscounted LIFO gain ($360), making LIFO better. But if Parcel 1 had been bought at $36.00 instead of $34.50, the FIFO gain would be $600, discounted to $300, and FIFO would beat LIFO ($300 taxable vs $360).

-

You have been buying on dips and your oldest parcels have the highest cost base. This happens when a stock dropped after your first purchase and you averaged down. Selling the high-cost first parcel under FIFO produces a smaller gain.

-

You want to preserve your newest parcels for future 50% discount eligibility. If Parcel 3 is only 6 months old, keeping it means it will qualify for the discount in another 6 months. Selling it now under LIFO means you lose that future benefit.

When LIFO Beats FIFO

LIFO tends to produce a better result when:

-

The stock has been trending up and your recent purchases are at higher prices. Selling higher-cost shares produces smaller gains.

-

None of your parcels qualify for the CGT discount (all held under 12 months). In that case, the only variable is the cost base, and you want to sell the highest-cost parcel. For swing traders holding positions for days to weeks, this is the common scenario.

-

You want to crystallise a small gain late in the financial year for tax planning, while preserving larger-gain parcels for the next year.

The Real Power: Specific Identification

For active swing traders, specific identification is the method worth understanding because it gives you flexibility FIFO and LIFO do not.

Consider a scenario where you hold three parcels: one at a loss, one at a small gain qualifying for the discount, and one at a large gain not qualifying. If you need to sell, specific identification lets you:

- Sell the loss parcel to offset gains elsewhere in your portfolio

- Sell the discounted parcel to minimise tax on the exit

- Defer the large undiscounted gain to next financial year if your income will be lower

Neither FIFO nor LIFO gives you this flexibility. The method is chosen by the rule, not by your tax position.

Record-Keeping Requirements

The ATO requires that you identify the specific parcel before or at the time of the sale -- not when preparing your tax return. In practice, this means:

- Maintain records showing each parcel separately (date, quantity, price, brokerage)

- At the time of sale, document which parcel you are disposing of

- Your broker statement may show only the average cost -- you need to maintain your own parcel register if using specific identification

- Keep records for 5 years after lodging the relevant tax return

Most brokers default to FIFO and do not offer parcel selection. If you use specific identification, you will need a separate system to track parcels and document your selections.

How SwingFolio Handles Parcel Tracking

SwingFolio records every trade entry and exit as a separate parcel with its own date, quantity, price, and brokerage. When you add partial exits to a position, the system maintains the link between each exit and the remaining parcels.

The tax report feature calculates the CGT impact using the parcel data you have recorded, letting you see the holding period and discount eligibility for each parcel. This gives you the information you need to make informed parcel selection decisions at the time of sale rather than scrambling to reconstruct records at tax time.

Practical Recommendations

For most swing traders whose average holding period is under 12 months:

- The 50% CGT discount rarely applies, so the holding period question is less relevant

- When all parcels are held short-term, the highest-cost parcel produces the lowest gain -- LIFO wins when the stock has been trending up, FIFO wins when you averaged down

- Specific identification gives you the most flexibility, but requires disciplined record-keeping

- If you do not want to maintain separate records, FIFO is the safest default because it is widely accepted and easy to audit

- Whichever method you use, be consistent and document it -- the ATO may question frequent switching between methods if it appears you are retrospectively optimising

The tax savings from choosing the right parcel selection method will not make or break your trading year. But across 50-100 trades, small differences per trade add up. Knowing your options and having the records to support your choices is part of running trading as a professional operation.

Disclaimer: This article is general information only and does not constitute financial or tax advice. Tax rules are complex and individual circumstances vary. The examples use simplified calculations and do not account for all possible factors (Medicare levy, HELP debt, offsets). Always consult a qualified tax professional for advice specific to your situation. The ATO's guidance on parcel identification is contained in Taxation Determination TD 33.