What Franking Credits Actually Are

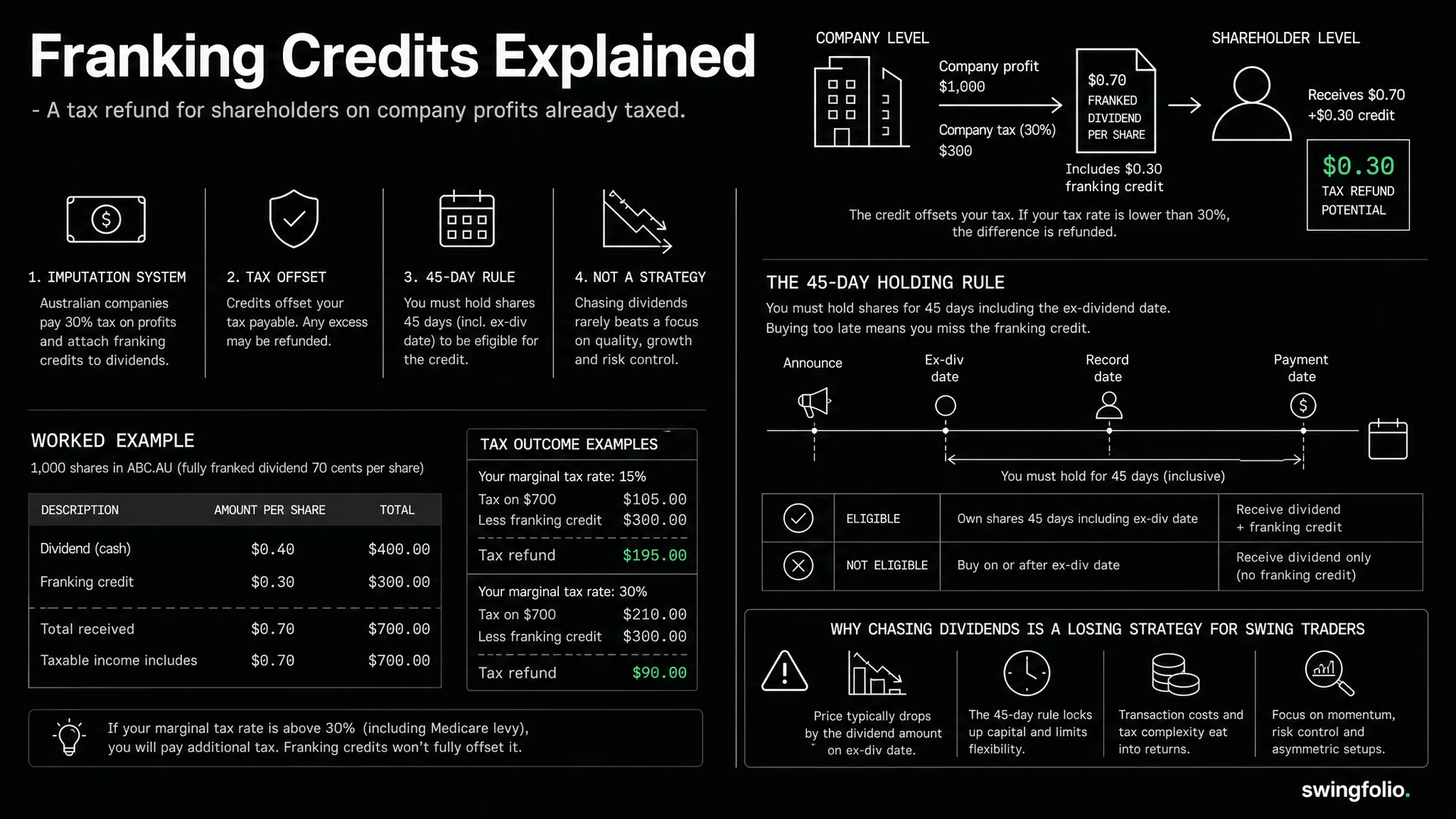

When an Australian company earns a profit, it pays company tax at 30% (or 25% for base rate entities with turnover under $50 million). When it distributes some of that after-tax profit as a dividend, the dividend comes with an attached credit representing the tax the company already paid. That attached credit is a franking credit, also called an imputation credit.

The system exists to prevent double taxation. Without it, the company pays 30% tax on its profit, then the shareholder pays their marginal tax rate on the dividend they receive -- taxing the same money twice. Franking credits give shareholders credit for the tax already paid at the company level.

Here is how the maths works for a fully franked dividend:

- Company earns $100 profit

- Company pays $30 tax (30% rate)

- Company distributes $70 as a fully franked dividend

- Shareholder receives $70 cash + $30 franking credit

- Shareholder includes $100 in their taxable income ($70 + $30 grossed-up amount)

- Shareholder's tax on $100 at their marginal rate (say 37%) = $37

- Less franking credit of $30

- Net tax payable by shareholder: $7

The effective tax rate on the dividend is 37% (the shareholder's marginal rate), not 37% on top of the 30% company tax. The franking system achieves single taxation at the shareholder's marginal rate.

Fully Franked, Partially Franked, and Unfranked

Not all dividends carry the same level of franking:

Fully franked: The company has paid the full 30% company tax on the profit being distributed. Most large ASX companies (CBA, BHP, CSL, Woolworths) pay fully franked dividends because they generate the majority of their profits in Australia where they pay Australian company tax.

Partially franked: The company has paid some company tax but not on the full amount. This happens when a company earns part of its profit overseas (where it pays foreign tax instead of Australian tax) or has tax losses offsetting some of its taxable income. A dividend might be described as "60% franked" meaning 60% of the dividend carries franking credits.

Unfranked: No franking credits attached. The company either paid no Australian tax on the distributed profit (common for companies with large overseas operations or carried-forward losses) or chose not to frank the dividend.

For a shareholder in the 37% bracket receiving a $1,000 dividend:

| Franking Level | Cash | Franking Credit | Gross Income | Tax (37%) | Net Tax | Effective Rate |

|---|---|---|---|---|---|---|

| Fully franked | $1,000 | $428.57 | $1,428.57 | $528.57 | $100 | 7.0% |

| 50% franked | $1,000 | $214.29 | $1,214.29 | $449.29 | $235 | 19.4% |

| Unfranked | $1,000 | $0 | $1,000 | $370 | $370 | 37.0% |

The tax difference between fully franked and unfranked is $270 on a $1,000 dividend. That is significant for investors holding shares for income. For swing traders, the picture is different.

The 45-Day Holding Rule

Here is where franking credits become largely irrelevant for active traders.

To claim a franking credit on a dividend, you must hold the shares "at risk" for at least 45 days. The 45-day period excludes the day you bought the shares and the day you sold them. The holding period must occur within a window starting 45 days before the ex-dividend date and ending 45 days after.

The "at risk" requirement means you cannot hedge away the price risk. If you hold the shares but also hold put options or short positions that reduce your exposure by more than 70%, the days where you are hedged do not count towards the 45 days. You must be genuinely exposed to the share price movement.

What This Means for Swing Traders

A typical swing trade lasts 3-20 trading days. Even a generous 20 trading days is only about 28 calendar days -- well short of the 45-day requirement. If you receive a dividend during a swing trade, you get the cash dividend but cannot claim the franking credit.

You still include the dividend in your income and pay tax on it at your marginal rate. You just do not get the offset. On a $500 fully franked dividend at the 37% marginal rate, losing the franking credit costs you $214.29 -- money the company already paid in tax that you cannot claim back.

The Small Shareholder Exemption

There is one exception. If your total franking credit entitlement for the entire financial year is $5,000 or less, the 45-day rule does not apply to you. You can claim all your franking credits regardless of how long you held the shares.

The $5,000 threshold refers to franking credits, not dividend income. At a 30% franking rate, $5,000 in franking credits corresponds to roughly $11,667 in fully franked dividends. Most swing traders will not hit this threshold because they are not holding positions through ex-dividend dates frequently enough.

However, if you also hold long-term investments that pay dividends (super, an investment portfolio, ETFs), those franking credits count toward the $5,000 total. If the combination of your long-term portfolio and any accidental swing trade dividends stays under $5,000 in franking credits, you can claim them all.

Note: the small shareholder exemption does not apply to SMSFs or trusts -- only individuals.

How Ex-Dividend Dates Affect Share Prices

On the ex-dividend date, the share price drops by approximately the amount of the dividend. If CBA closes at $110.00 the day before going ex-dividend, and the dividend is $2.50, the theoretical opening price on the ex-date is $107.50.

In practice, the drop is often slightly less than the full dividend amount because the franking credit has value. Studies of ASX stocks show the average ex-date price drop is around 75-85% of the total dividend (cash plus franking credit value), though this varies by stock, market conditions, and the prevailing franking credit value at different tax rates.

For swing traders, this creates two practical considerations:

Holding through ex-dividend: If your swing trade spans an ex-dividend date, the price drop can look like a sudden loss on your chart. Your P&L on the share price declines, but you receive the dividend as cash separately. Your total return (capital plus dividend) may be neutral or positive, but your chart-based stop loss might trigger on what is just a mechanical price adjustment.

Trading the ex-dividend drop: Some traders try to buy before ex-dividend and sell after, capturing the dividend. This strategy rarely works for swing traders because:

- The share price drops by roughly the dividend amount, so you do not gain from the price

- You do not qualify for the franking credit (held less than 45 days)

- The net effect is that you receive a cash dividend but lose it on the share price drop, and you owe tax on the dividend at your full marginal rate without the franking offset

The maths does not work. Do not change your swing trading strategy around dividend dates.

Franking Credits in SMSFs

Self-managed super funds in accumulation phase pay tax at 15%. For fully franked dividends, the franking credit (30%) exceeds the fund's tax liability (15%), resulting in a refund of the excess 15%.

Using the earlier example of a $1,000 fully franked dividend:

- Gross-up amount: $1,428.57

- Tax at 15%: $214.29

- Franking credit: $428.57

- Net result: refund of $214.28 to the fund

This is why fully franked dividends are popular in SMSF strategies -- the fund effectively receives more than the cash dividend after the franking credit refund.

For SMSF pension phase, income (including dividends) is generally tax-free, so the entire franking credit is refunded. A $1,000 fully franked dividend in pension phase returns $428.57 in franking credit refunds, making the total receipt $1,428.57.

However, the 45-day rule still applies to SMSFs (the small shareholder exemption does not apply to super funds). An SMSF engaged in short-term trading would need to hold shares at risk for 45 days to claim the franking credits. For swing trading within an SMSF, the same limitation applies as for individual traders.

Practical Advice for Active Traders

Franking credits are a tax feature designed for long-term shareholders. For swing traders:

-

Do not adjust your strategy for dividends. The franking credit system rewards long holding periods. Swing trading rewards short holding periods. These are fundamentally different approaches, and trying to combine them usually produces worse results than committing to either one.

-

Be aware of ex-dividend dates on your watchlist. Not to trade around them, but to avoid confusion when a stock gaps down on the ex-date. Adjust your stop loss calculations to account for the expected dividend drop if you are holding through an ex-date.

-

Check the $5,000 small shareholder threshold. If you accidentally receive dividends on swing trades and your total franking credits for the year are under $5,000, you can still claim them without meeting the 45-day rule. Track this during the year.

-

Record all dividend income. Even if you cannot claim the franking credit, you must report the dividend as income. Your broker will provide a tax statement showing dividend income received, and the ATO receives this data directly from your broker.

-

Keep franking credits and trading strategy separate in your thinking. If you want dividend income with franking credits, build a separate long-term portfolio. Do not contaminate your swing trading decisions with dividend considerations.

The trading edge you develop through swing trading -- entries, exits, position sizing, risk management -- is worth far more than any franking credit. Stay focused on what you are good at.

Disclaimer: This article is general information only and does not constitute financial or tax advice. Tax rules are complex and individual circumstances vary. The examples use simplified calculations and do not account for all possible factors. The 45-day rule has additional complexities around related payments and delta hedging that are beyond the scope of this article. Always consult a qualified tax professional for advice specific to your situation.