Where Capital Gains Go on Your Tax Return

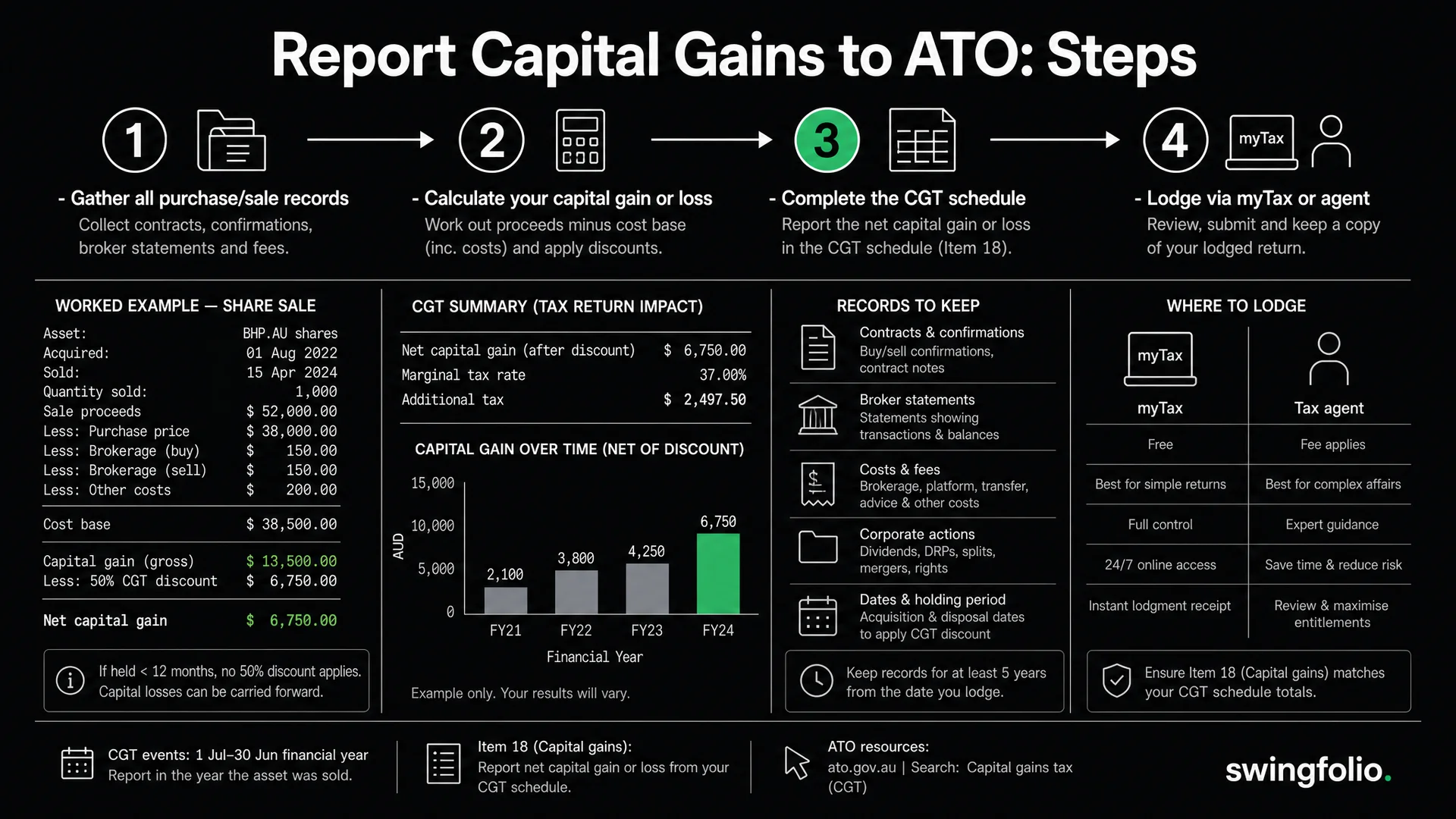

Capital gains are reported at Item 18 of the individual supplementary tax return. If you use myTax (the ATO's online lodgement system), the capital gains section is under "Income" in the Australian income or losses from investments or property section.

Item 18 asks a series of questions that determine how much detail you need to provide. The basic question is whether you had any CGT events during the financial year. If yes, you work through the labels to report your total current year capital gains, apply losses, apply the discount if applicable, and arrive at your net capital gain.

The net capital gain figure is what gets added to your other taxable income (salary, business income, interest, dividends) and taxed at your marginal rate.

Do You Need a CGT Schedule?

The CGT schedule is a more detailed form that breaks down your capital gains by category, method, and discount eligibility. You must complete and lodge a CGT schedule if:

- Your total current year capital gains are greater than $10,000, or

- Your total current year capital losses are greater than $10,000, or

- You choose to use the indexation method for assets acquired before 21 September 1999, or

- You have a net capital loss from a collectables category

Most active share traders will trigger the $10,000 threshold for gains or losses across the year. If you made 50 trades with an average gain of $300, your total gains are $15,000 and you need the schedule. The threshold is based on total gains (or total losses), not net gain.

If your total gains and losses are each under $10,000, you can report just the net capital gain at Item 18 without the detailed schedule.

The Step-by-Step Process Using myTax

Here is the actual sequence when lodging through myTax:

Step 1: Access the Capital Gains Section

Log in to myGov and navigate to myTax. Under "Income", select "Capital gains". If you have data from share registries or crypto exchanges that has been pre-filled by the ATO, it will appear here. Check it carefully -- pre-fill data is often incomplete or uses cost bases that do not match your records.

Step 2: Answer the Qualifying Questions

myTax asks whether you had CGT events during the year and whether your total gains or losses exceed $10,000. Answer honestly. Answering "no" when you had CGT events is one of the most common errors flagged in ATO audits.

Step 3: Enter Your Capital Gains by Category

If you need the CGT schedule, you categorise your gains:

- A1: Total current year capital gains from CGT assets and CGT events (shares, crypto, property, other assets)

- A2: Attributed gains from trusts and managed funds (if applicable)

For share traders, the bulk goes into A1. You report the total gains, not individual trades. Your supporting records (trade journal, broker statements) contain the individual trade details.

Step 4: Apply Capital Losses

This is where you reduce your gains:

- Current year capital losses: Losses from trades closed during the same financial year. These offset gains dollar-for-dollar with no limit.

- Prior year net capital losses: If you had a net capital loss in a previous year, you carry it forward and apply it against this year's gains. Capital losses can be carried forward indefinitely but cannot be carried back.

Capital losses are applied to gains in a specific order:

- Apply losses against gains that do NOT qualify for the CGT discount first

- Then apply remaining losses against discounted gains

This ordering maximises the benefit of the discount. By reducing non-discounted gains first, more of the discounted gains survive at the 50% rate.

Step 5: Apply the CGT Discount

After subtracting losses, apply the 50% discount to any remaining gains from assets held over 12 months. The system calculates this automatically if you have entered the holding period information correctly.

Remember: the discount is applied AFTER losses, not before. The correct formula is:

Net capital gain = (Total gains - Total losses) x discount percentage for eligible gains

Step 6: Review and Lodge

The final net capital gain figure flows into your taxable income. Review the calculation, confirm your figures match your records, and lodge.

What Information Goes Where

Here is a mapping of common label fields in the CGT schedule:

| Label | What It Contains | Example |

|---|---|---|

| Total current year capital gains | Sum of all capital gains before losses | $18,500 |

| Net capital losses carried forward to later years | Unused losses from this year | $0 |

| Net capital gain | Final amount after losses and discount | $7,250 |

| Net capital losses applied | Losses used to offset gains this year | $4,000 |

The net capital gain at the bottom of Item 18 is what appears in your taxable income. If you have a net capital loss for the year (losses exceed gains), you carry it forward -- it does not reduce your other income.

Using myTax vs a Tax Agent

Both options produce the same tax outcome if the numbers are correct. The choice depends on your complexity and confidence.

myTax works well when you trade only ASX shares or a small number of crypto assets, have clean records with clear cost bases, and your total transactions are under 50-100 per year. It is free, lodgement is immediate, and ATO pre-fill speeds up data entry. The risk is that no one reviews your calculations -- errors in cost base, discount eligibility, or loss ordering may not surface until an audit.

A tax agent is worth the cost when you have hundreds of trades per year, trade across multiple asset classes, have foreign income or multi-currency considerations, or are unsure whether you qualify as a trader or investor. Expect $300-$800 for a moderately complex return. A competent agent catches errors, applies optimisations, and provides a defensible position if audited.

For active traders in their first year or two, using a tax agent at least once establishes the correct approach that you can replicate in subsequent years using myTax.

What Records to Keep and for How Long

The ATO requires you to keep records for 5 years after lodging the tax return for the income year the transaction relates to. For a trade made in the 2025-26 financial year, you lodge your return by October 2026 (or March 2027 via a tax agent), and records must be kept until October 2031 or March 2032.

For CGT assets you still own, you must keep acquisition records for the entire period of ownership plus 5 years after the disposal and lodgement of the relevant return. If you bought shares in 2020 and sell them in 2030, you keep the 2020 purchase records until at least 2035.

Records You Need for Each CGT Event

- Date of acquisition and date of disposal

- Cost base (purchase price plus brokerage, fees, and incidental costs)

- Sale proceeds (minus selling costs)

- Holding period (for CGT discount eligibility)

- Method used to identify parcels (FIFO, LIFO, specific identification)

- Any adjustments to cost base (corporate actions, return of capital, share splits)

Where These Records Come From

Broker trade confirmations are your primary source for share trades -- download and store them rather than relying on your broker indefinitely. For crypto, export CSV files from each exchange at least annually. Blockchain transaction hashes provide on-chain records for DeFi activity.

SwingFolio maintains a detailed record of every trade entry, exit, and partial position, including dates, prices, fees, and holding periods. The CGT report feature generates a summary formatted for Australian tax reporting, giving you the data you need for Item 18 and the CGT schedule.

Common Mistakes That Trigger ATO Attention

1. Not Reporting Crypto Disposals

The ATO's data-matching program cross-references exchange data with tax returns. If your exchange records show $50,000 in crypto disposals but your tax return shows no CGT activity, expect a letter. This is the single most common crypto-related audit trigger.

2. Applying the Discount Before Losses

As covered above, the correct order is: gains minus losses, then apply discount. Applying the discount first and then subtracting losses produces a lower taxable gain and is incorrect. The ATO's systems check for this pattern.

3. Not Reporting Small Gains

There is no minimum threshold below which capital gains are tax-free for individuals (unlike the $10,000 personal use asset rule, which has specific conditions). A $50 gain on a quick share trade is still a capital gain and should be reported.

4. Incorrectly Claiming the CGT Discount

Claiming the 50% discount on assets held for less than 12 months. This happens when traders count business days instead of calendar days, or do not account for the "12 months plus one day" rule correctly. The ATO checks holding periods against acquisition dates reported by registries.

5. Forgetting to Carry Forward Losses

If you had a net capital loss last year and forgot to record it, you miss the offset against this year's gains. Capital losses carry forward indefinitely, but you need to track them. Your prior year tax return shows your carried-forward loss balance -- check it before preparing this year's return.

6. Missing Corporate Actions

Share splits, consolidations, demergers, and return-of-capital payments all adjust your cost base. A return of capital reduces your cost base (it is not a dividend). If you do not adjust for it, you will understate your gain when you eventually sell. Check your share registry statements and ASX announcements for any corporate actions on stocks you held during the year.

Timeline and Deadlines

| Date | What Happens |

|---|---|

| 30 June | Financial year ends. All CGT events up to this date go on this year's return. |

| 1 July - 31 October | Lodgement period for self-lodgement via myTax |

| 1 July - 15 May (next year) | Extended lodgement period if using a registered tax agent |

| ATO pre-fill available | Usually mid-August for share data, later for crypto |

| 5 years after lodgement | Minimum record retention period |

If you self-lodge, aim to lodge in September or October once pre-fill data is available and you have all broker and exchange statements.

Disclaimer: This article is general information only and does not constitute financial or tax advice. The ATO updates forms and procedures annually -- verify current requirements on ato.gov.au for the relevant income year. Tax rules are complex and individual circumstances vary. Always consult a qualified tax professional for advice specific to your situation.