The biggest IPO in history meets the oldest pattern in markets

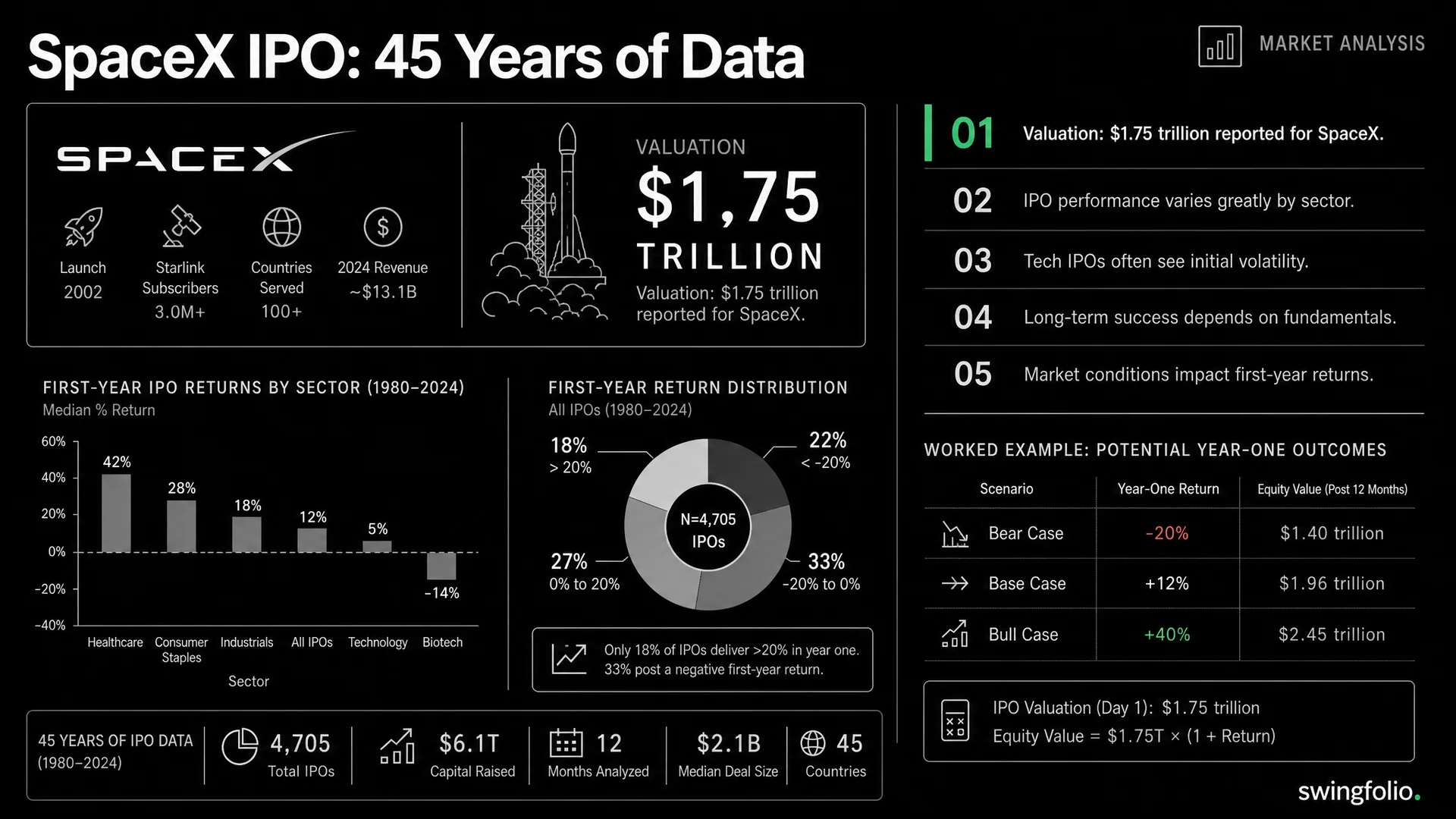

In May 2026, SpaceX filed a draft registration statement, an S-1, with the U.S. Securities and Exchange Commission to list on the Nasdaq under the ticker SPCX. The terms are large enough to reset the record books: a target valuation of about $1.75 trillion to $2 trillion and a raise around $75 billion. Price it anywhere close to that and it becomes the largest initial public offering in history by a wide margin. Saudi Aramco set the prior record in 2019 at about $29 billion. SpaceX wants to raise more than twice that.

Two questions matter more than the headline. What are you buying? And what does the historical record say about how IPOs, especially the very largest ones, trade in their first 12 months? Both deserve an answer, drawn from the filing as reported and from 45 years of academic IPO data. None of this is a recommendation. It is context for a deal that will dominate the financial press for months.

One caveat on the numbers below. They come from press coverage of a draft S-1, including a Reuters review of the filing, ahead of the final prospectus and pricing. Figures move before a deal prices. Read them as a close approximation, not the last word.

Inside the S-1

Strip away the spectacle and the filing describes three different businesses bolted onto one income statement.

Starlink, the satellite-internet utility. This is the engine. Starlink generated about $11.4 billion in revenue in 2025 and $4.42 billion in operating income, serving an estimated 10.3 million subscribers. A recurring-revenue connectivity business with margins like that is the part of SpaceX that resembles a maturing, profitable company.

The launch business. Falcon and the wider launch operation added $4.1 billion in revenue. SpaceX puts more mass into orbit than all other launch providers combined, and that business pays for much of the rest.

xAI, the artificial-intelligence lab. Most headlines skip the third business, and that changes how you read the numbers. In February 2026, Musk folded his AI company, xAI, into SpaceX in an all-stock deal that valued the combined entity at about $1.25 trillion at the time. xAI added $3.2 billion of revenue in 2025 but, according to the filing, drives almost the entire consolidated net loss through its capital spending and operating burn. One account put xAI's cash burn around $6.4 billion the year before.

Together, the combined company reported $18.67 billion in revenue for 2025, up about a third from $14.1 billion in 2024, and a net loss of $4.94 billion. A year earlier, on a standalone basis, SpaceX earned an estimated $791 million. Capital spending ran near $20.7 billion in 2025, which shows how much cash this machine consumes.

Look only at the consolidated loss and you miss the most important fact in the document: two of the three businesses make money. The data centers create the loss. The rockets and Starlink throw off cash.

The Anthropic wrinkle

In May 2026, SpaceX signed cloud-services agreements with Anthropic for access to its Colossus compute infrastructure, the Colossus and Colossus II data centers, the first in Memphis, Tennessee. The terms have Anthropic paying about $1.25 billion a month through May 2029, about $15 billion a year and up to $45 billion across the full term.

Weeks before filing, SpaceX locked in a named, paying, enterprise-scale customer for its AI division, and that customer competes head-to-head with xAI. A bull sees a speculative AI story turning into contracted revenue. A skeptic sees how circular and capital-hungry the current AI-infrastructure boom has become.

The price tag

At $1.75 trillion on $18.67 billion of 2025 revenue, you pay about 94 times trailing sales. At the top of the range, $2 trillion, you pay closer to 107 times. For context, most of the largest companies on earth trade in the single digits to low teens on sales. Nvidia, at the peak of the AI boom, traded in the 30s to 40s. A multiple in the 90s is venture-capital pricing stretched across a near-trillion-dollar base.

Isolate the profitable core, Starlink and launch at about $15.5 billion of combined revenue, and the picture barely improves: you still pay well over 100 times that core's own sales, with the loss-making AI lab thrown in as an option on the future. The raise of $75 billion against a $1.75 trillion value means the company floats only about 4 percent of its shares. A thin free float against heavy index-driven demand can swing hard in both directions.

You are buying three things at once: a profitable space company, a launch franchise, and a money-losing AI bet, priced together at a level that needs almost everything to go right.

One man holds the votes

Through a dual-class structure, Musk owns about 42 percent of the equity and controls roughly 85 percent of the voting power. The Class B shares carry ten votes each; the Class A shares sold to the public carry one. You buy economic exposure, not a say. Governance researchers have tracked how dual-class structures draw a valuation discount over time, because outside owners cannot discipline management. With a founder as singular as Musk, that doubles as the bull case and the bear case: you bet on one person, and you cannot vote him out.

The historical record on IPOs

Set the hype aside and look at the data. Jay Ritter of the University of Florida has tracked every significant U.S. IPO since 1980, a dataset of more than 9,000 offerings updated through the end of 2025. Start with the first day, then the first year.

The first-day pop is real, and it mostly pays insiders and allocated investors. From 1980 to 2025, the average IPO rose about 19 percent on its first day from the offer price to the first close, with a median of 7 percent. That gain goes to whoever lands an allocation at the offer price, and for a hot deal the buyers are institutions, not retail traders clicking buy on the open. Big deals pop far less than the average, closer to 10 percent, because underwriters scrutinize and price them with more care. Technology IPOs run hotter, averaging a first-day return above 30 percent, which cuts both ways for an AI-flavored offering.

Over the first 12 months, the average IPO makes a little and lags a lot. Measured from the first day's closing price, the average U.S. IPO from 1980 to 2024 returned about 5.6 percent over its first year, but trailed a broad market index by about 5.8 percent across that same year. A small nominal gain, and a clear miss against the alternative of owning the index. The average also buries enormous variation by era:

| IPO cohort | Average 1-year return (from first close) | Versus the market |

|---|---|---|

| 1980 to 1989 | +3.4% | -3.6% |

| 1990 to 1999 | +14.9% | -0.9% |

| 2000 to 2009 | -11.3% | -19.7% |

| 2010 to 2024 | -0.8% | -9.4% |

| 1980 to 2024 | +5.6% | -5.8% |

The 1990s cohort rode a bull market to strong raw returns. The 2000s cohort, caught between the dot-com bust and the financial crisis, lost money outright and trailed the market by nearly 20 points in year one. The most recent stretch, 2010 to 2024, averaged a slightly negative first year and a 9-point miss against the index. Regime matters as much as the company.

Stretch the horizon and the gap widens. Over three years from the first close, the same dataset shows an average buy-and-hold return of 19.1 percent but a market-adjusted return of negative 20.5 percent, near 5.5 percent of underperformance a year. The longer you hold the average IPO, the more it costs you against a simple index.

Size and profitability split the field. The averages hide the one distinction that has paid:

- IPOs of companies with more than $1 billion in revenue have matched the market over three years, a style-adjusted return of about positive 0.6 percent, while small issuers trailed by a wide margin.

- Profitable issuers matched or beat their peer group, a style-adjusted return of about positive 1.8 percent, while unprofitable issuers trailed by more than 23 percent.

So where does SpaceX land? Enormous on revenue, which is the good bucket. Unprofitable on a consolidated basis, which is the bad bucket, and that loss traces back to xAI. The record refuses to hand you a clean verdict. You can read its revenue as a reason it works and its losses as a reason for caution, and both readings hold.

The cautionary cohort: 2020 and 2021

For a reminder of what happens when hype meets a cold market, look at the SPAC and IPO boom of 2020 and 2021. Ritter's figures on the 451 companies that went public via SPAC merger from 2012 to 2022 show an average return of about negative 46 percent in the first year alone, against a market up about 3 percent over the same windows. The 2021 vintage averaged about negative 64 percent in year one. Buyers paid for a story about a vast future market and very little present profit. The parallel to an AI lab valued on its potential is not exact, but hold it in mind.

Year one: the record of the giants

Averages hide the thing that decides a single name: dispersion. To see it, look at a basket of 30 well-known technology and growth IPOs from the past decade, tracked from their first close out to one year.

The first pattern is a fade. Most of these names traded higher in their opening weeks, then rolled over as the early enthusiasm drained:

| Time after IPO | Median return | Share finishing positive |

|---|---|---|

| 1 week | +3% | 57% |

| 1 month | +1% | 57% |

| 3 months | +4% | 57% |

| 6 months | -9% | 43% |

| 12 months | -9% | 43% |

Through the first three months, most of the basket sat in the green. By six months the median name was underwater, and it stayed there at 12 months. The average 12-month return looks friendlier at about positive 14 percent, but a few monster winners pull that average up over a long tail of losers. For a name picked at random, the median is the honest number.

Now the names themselves, ranked by 12-month return, alongside the deepest drawdown each one put its first-year holders through:

| Company | 12-month return | Year-1 max drawdown |

|---|---|---|

| Palantir | +153% | -53% |

| Zoom | +142% | -40% |

| Arm Holdings | +132% | -43% |

| Datadog | +128% | -42% |

| MongoDB | +103% | -26% |

| Cloudflare | +90% | -32% |

| CoreWeave | +87% | -65% |

| Okta | +64% | -20% |

| CrowdStrike | +64% | -67% |

| Snowflake | +27% | -52% |

| Airbnb | +25% | -39% |

| Twilio | +3% | -66% |

| Shopify | +2% | -52% |

| Spotify | -3% | -46% |

| Block | -7% | -44% |

| -10% | -58% | |

| DoorDash | -13% | -47% |

| Uber | -21% | -68% |

| Dropbox | -24% | -54% |

| Affirm | -26% | -65% |

| Snap | -26% | -56% |

| -28% | -70% | |

| Alibaba | -30% | -49% |

| -31% | -54% | |

| Roblox | -40% | -69% |

| Coinbase | -55% | -57% |

| Coupang | -65% | -64% |

| Lyft | -65% | -79% |

| Rivian | -67% | -88% |

| Robinhood | -74% | -90% |

| Basket median | -9% | -54% |

| Basket average | +14% | -55% |

Two things stand out.

First, the winners share a trait. The names that compounded, Palantir, Zoom, Arm, Datadog, MongoDB, Cloudflare, CrowdStrike, ran real, growing, often profitable software and chip businesses. The names that fell hardest, Robinhood, Rivian, Coinbase, Coupang, Lyft, sold a story about a future market far ahead of present economics. SpaceX carries both traits at once: a profitable space-and-satellite core and an AI bet priced far ahead of its fundamentals.

Second, read the drawdown column. Even the standout winners put their holders through deep declines. Arm fell 43 percent at its worst inside a year it finished up 132 percent. CrowdStrike drew down 67 percent. CoreWeave, the 2025 AI-infrastructure listing closest to SpaceX in spirit, ended year one up 87 percent after a 65 percent drawdown. Across the whole basket, the median worst-drawdown was about 54 percent. A strong long-run outcome and a punishing first year often live in the same stock.

The lockup: a date to circle

One mechanical feature shapes the first year of almost every IPO. The lockup period, usually 180 days, bars insiders and pre-IPO investors from selling. When it lifts, fresh supply hits the market. Studies find negative abnormal returns clustered around lockup expiry, on the order of negative 1.5 to negative 2.5 percent in the days around it, with the largest effect in venture-backed names that ran up hard after listing. For a June 2026 listing, the first major supply test lands around December 2026. This is a scheduled event, not a forecast.

How a disciplined trader frames it

For an active trader, a deal like this raises practical questions, even though nothing here tells you what to do.

The first days turn on supply and demand, not value. A thin float and heavy index-inclusion buying produce violent two-way moves that have little to do with discounted cash flows. The opening print reflects positioning and scarcity as much as fundamentals.

The base rates stay knowable even when the outcome does not. History says the largest IPOs disappoint about as often as they deliver in year one, that the first-day pop mostly pays allocated insiders, and that insiders can sell for the first time around the six-month mark, which can flood the market with stock. Even the basket names that ended year one higher drew down a median of about 54 percent first. None of that fixes where SPCX trades next week. All of it widens the range of outcomes you should expect.

Risk per trade stays the one variable you control. You cannot control whether a $1.75 trillion business compounds or de-rates. You can control how much you put at risk on a single position and where your exit sits before you enter. A structured trading journal enforces that discipline: defining risk in advance, sizing to it, and checking afterward whether you followed the plan. A deal this loud is the setting where pre-defined risk earns its keep, because the pull to chase runs strongest.

The bottom line

On the reported terms, the SpaceX IPO is the largest in history and one of the most fascinating businesses ever to come public: a profitable satellite utility and a dominant launch franchise, wrapped around a cash-burning AI lab, priced at about 94 times sales, with a founder who keeps near-total voting control. The bull case rests on real optionality across space, connectivity, and AI. The bear case rests on a valuation that prices in a near-flawless future and a consolidated loss the headline multiple glosses over.

The record will not tell you the answer. It will tell you that the average IPO lags the market in year one, that the very largest deals disappoint about as often as they deliver, that revenue scale and profitability separate the long-run winners from the losers, and that even the winners tend to draw down 40 to 65 percent before they pay off. SpaceX carries the trait that has worked, enormous revenue, alongside the trait that has not, consolidated losses. The hype will fade within a few weeks, and that underlying tension will still be sitting there.

This article is general information and market analysis, not personal financial or investment advice. It is not a recommendation to buy, sell, or hold any security, including SPCX or any SpaceX-related instrument. Figures come from press coverage of a draft registration statement as of May 2026, and from the IPO research of Jay Ritter at the University of Florida, and may change. Do your own research and consider professional advice for your circumstances.