Tax-loss selling is the practice of selling a losing share before 30 June so the capital loss can offset capital gains you booked the same year. It is legal, and badly misunderstood.

The mistakes are rarely in the selling. They sit in what people do next, and in believing the loss does more for the tax bill than it actually does.

General information only. Not financial or tax advice.

What is tax-loss selling?

Tax-loss selling means disposing of an asset at a loss to crystallise a capital loss, then using that loss to reduce capital gains in the same financial year. Some people call it tax-loss harvesting. It is the same thing.

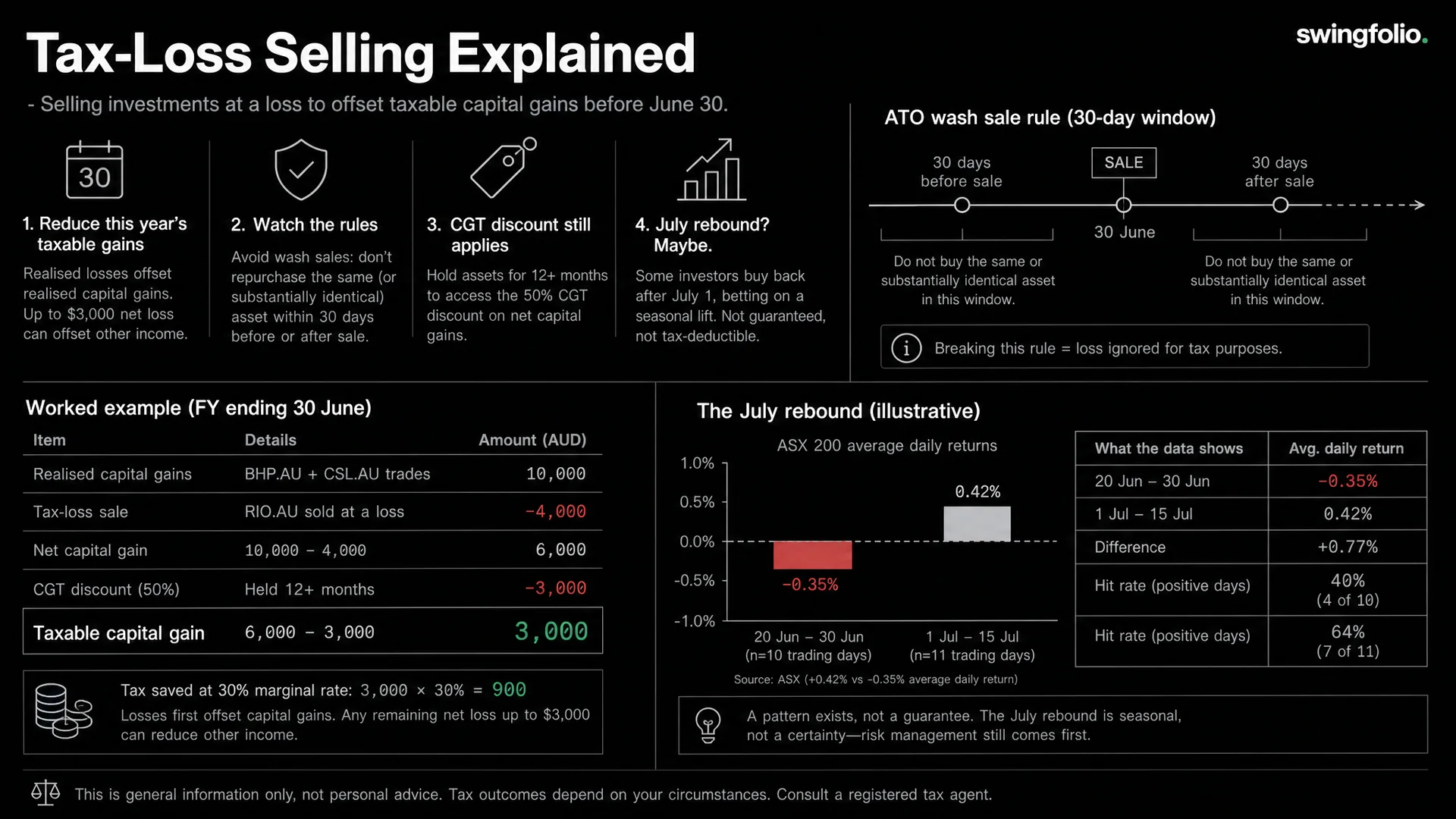

The word that matters is crystallise. A loss on paper does nothing for your tax. The ATO is blunt about it: you can only claim a loss on shares you have actually disposed of, not on investments you still hold. Until you sell, the loss is unrealised and the ATO does not see it.

The trade itself is simple. You hold a share that is underwater. You have a capital gain elsewhere this year. You sell the loser, the loss becomes real, and it cancels out part of the gain.

How does a capital loss actually cut your tax?

A capital loss can only offset a capital gain. It cannot reduce your salary, your interest, or any other income. If your losses for the year are larger than your gains, the surplus becomes a net capital loss that carries forward, with no time limit, until you have future gains to use it against.

That one rule corrects a common assumption. A $5,000 loss does not hand you $5,000 back. It lowers the gain you pay tax on. The benefit is the tax you would have paid on that slice of gain, not the loss itself.

The order of operations matters more than most people realise, and it is where real money is won or lost. The ATO applies capital losses to your gains before the 50% CGT discount, and it tells you to subtract losses from any non-discounted gains first.

A quick example shows the gap. Say you have a $10,000 gain on shares held longer than 12 months, a $4,000 gain on shares held three months, and a $4,000 loss to use.

- Put the loss against the short-held gain first. That gain falls to $0. The $10,000 long-held gain then gets the 50% discount, leaving $5,000 taxable. Total taxable: $5,000.

- Put the same loss against the long-held gain instead. That gain drops to $6,000, the discount halves it to $3,000, and the untouched $4,000 short gain stays in full. Total taxable: $7,000.

Same loss, $2,000 difference in what you are taxed on. Losses go against the gains that do not get the discount first. For the detail on who qualifies for the discount and how the 12-month clock works, see our guide to the 50% CGT discount.

When is the cut-off to sell before 30 June?

For listed shares, the capital gain or loss falls in the financial year of the trade date, not the settlement date. The CGT event happens when your order executes on market, not two business days later when the trade settles.

Plenty of investors get caught by this. ASX trades settle on a T+2 basis, so a sale executed on 30 June settles in early July. The cash lands in the new financial year, but the loss belongs to the old one, because the trade date is what counts.

The day your sell order fills is the day that decides which year the loss lands in. Leaving it to the final minutes of 30 June carries its own risk, because an order that does not fill is a loss you cannot claim this year. That is an observation about timing, not a suggestion to trade.

What is the ATO wash-sale rule?

Sell a share to bank the loss, then buy it straight back, and the ATO can cancel the loss. This is what the ATO calls a wash sale, and it is the fastest way to turn a legitimate tax move into a problem.

Taxpayer Alert TA 2008/7 describes a wash sale as an arrangement where an asset is disposed of but there is no substantial change in economic interest in it. In plain terms, you sold, but your position did not change in substance, and the dominant reason was the tax benefit.

The ATO spells it out with its own example. A taxpayer sells 50,000 shares to crystallise a $62,000 loss, then buys the same 50,000 shares back the next day. The regulator treats the sale and 24-hour repurchase as a single scheme whose dominant purpose was the loss, and the Commissioner can cancel that tax benefit under Part IVA. Penalties of up to 50% of the tax avoided can apply.

Australia has no fixed waiting period. The United States has a bright-line 30-day rule. We do not. The test here is your dominant purpose and whether your economic exposure changed in substance, not a number of days on a calendar. Selling out of a position for real, and being free to buy back later if your view changes, is different from a pre-planned round trip designed to manufacture a loss. For where that line sits and how to stay on the right side of it, read our breakdown of wash sale rules in Australia.

Is the July rebound real?

There is real research behind a July seasonal pattern on the ASX, but it is narrower than the market chatter suggests. The idea is that stocks dumped in June for tax reasons bounce back in July once the selling pressure clears.

The academic anchor is a 1983 study by Brown, Keim, Kleidon and Marsh in the Journal of Financial Economics. Because Australia's tax year ends on 30 June, they found a July seasonality consistent with tax-loss selling, and it showed up most strongly in small stocks. It is the local cousin of the United States January effect, where the tax year ends in December and the bounce tends to come in January.

A Stanford working paper is more cautious. It notes tax-loss-selling predictions are ambiguous, because other forces can offset the effect. The pattern is documented, then, but it is concentrated in smaller companies, and it is not a dependable whole-market rule you can lean on.

You will also see the claim that the June tax-loss trade "works 72% of the time since 2000." That figure traces to market commentary, not to any study I could find. Treat it as lore until someone shows the data and the method behind it.

I read it as real enough to know about, and too soft and too concentrated in small caps to trade as a sure thing. A seasonal tailwind that might exist is not an edge.

How do you stop tax trades from skewing your numbers?

A trade you make for tax reasons is not a trade you made because the setup was good. Mix the two in one journal and your performance stats drift.

Suppose you sell three positions in late June to harvest losses. Log them as normal exits and your win rate drops, your average loss grows, and the strategy that fed them looks worse than it is. None of that reflects how you trade.

The fix is to keep tax-motivated trades in their own bucket. In Swingfolio you can tag a trade as a tax-loss sale, so your strategy analytics still measure your real edge and your end-of-year capital gains stay easy to report. Now your numbers reflect your trading, and the tax housekeeping sits to one side.

Tax-loss selling FAQ

Is tax-loss selling legal in Australia? Yes. Selling a share at a loss to offset a capital gain is legal and ordinary. What is not allowed is selling and then buying back the same position mainly to manufacture the loss, which the ATO treats as a wash sale.

Can I sell shares at a loss and buy them back the next day? It is risky. The ATO's own example treats a 24-hour buyback as a scheme it can cancel under Part IVA, with penalties of up to 50% of the tax avoided. There is no safe number of days in Australia. What matters is your dominant purpose and whether your position changed in substance.

Can a capital loss reduce my salary or other income? No. Capital losses offset capital gains only. If your losses exceed your gains, the surplus carries forward with no time limit until you have future gains to use it against.

When is the cut-off to sell before the end of the financial year? The trade date sets the year. A sale executed by 30 June counts for that financial year even though it settles in early July under T+2.

Does the 50% CGT discount come off before or after losses? Losses come off first. You subtract capital losses from your gains, then apply the 50% discount to what is left, and you get the best result by using losses against gains that do not qualify for the discount first.

Where this leaves you

Tax-loss selling is a legitimate tool with hard limits. Done properly it means a real sale, losses applied to your least-discounted gains first, an eye on the trade date around 30 June, and no same-position buyback. The July rebound is a footnote worth knowing, not a strategy to bet on.

For the full pre-30-June run sheet, our end of financial year tax checklist for Australian traders walks through it step by step.

General information only. Not financial or tax advice. Tax outcomes depend on your circumstances. Check with a registered tax agent or the ATO before acting.